The Missing Unit

An 11-year AWS veteran on why alternative protein's real bottleneck is financial, not biological.

Hey there! 👋

Skander here.

The standard story about alternative protein is that demand fell short. True, but incomplete.

Scott Renda spent 11 years at AWS watching primitives, public pricing, and pay-as-you-go turn cloud computing into something a lender could underwrite. Now he’s pointing that same lens at fermented protein, and the diagnosis is uncomfortable.

Renda’s argument is that the deeper bottleneck is financial: fermentation capacity can’t be priced, compared, or underwritten the way infrastructure assets are in mature sectors. There’s no shipping container for a liter of bioreactor time. Most CDMOs run a “contact us” model, contracts hide pricing inside private MSAs, and a lender staring at one signed number learns what one buyer paid, not what the next vessel earns.

His proposed fix, the “Protein Fabric,” is three moves in parallel: define the standardized units of work, post the prices publicly, and offer more than one way to buy. He then runs a repeatable method across all three production stages (feedstock and strain, fermentation, downstream processing) to actually pick the primitives, and builds a working rate card to show what it looks like priced.

It’s a technical and deliberately falsifiable piece. Scott Renda is new to the space and says so repeatedly, inviting you to tell him where he’s wrong.

Proof him wrong, or fix alternative protein with him.

🌊 Let’s dive in

1. Intro

Picture a steel box, eight feet wide, stacked ten high on a ship the length of four football fields, so familiar it no longer registers as special. Yet those boxes reoriented the global economy. Before the shipping container, moving goods across oceans was a custom nightmare of barrels, crates, and prices quoted dock by dock. By standardizing the unit of work, the maritime industry made the infrastructure legible enough that trade could finally scale, and the capital to build it could finally be raised.

Right now, fermented proteins (precision, biomass) are stuck before their own shipping container moment. Many people know fermentation makes food staples like bread, beer, and cheese: a living thing like yeast, bacteria, or fungi feeds on simple ingredients and turns them into something new. Far fewer know the same process, targeted at a specific protein, can make egg and meat proteins, grow protein-rich biomass like mycoprotein, or produce dairy’s whey and casein found, without the cow.

In the first part of this decade, startups such as Meati, Beyond Meat, Perfect Day, and Believer Meats1 chose to build their own facilities, owning their destiny rather than relying on tolling suppliers or food-grade Contract Development and Manufacturing Organizations (CDMOs). Then consumer demand for alternative proteins fell well short of expectations, breaking two things: the companies that built their own infrastructure couldn’t reach the scale that drives unit-economic improvement, and the capital that could have funded shared, multi-tenant capacity (third party) never materially showed up.

Breaking through this wall is the thesis Liberation Bioindustries3 was founded on and why they are commissioning a 600K-liter facility this year in Indiana. But a pioneer facility cannot carry an entire industry, especially when the commercial-scale capacity startups want today would have been financed and commissioned in 2021-2024, when venture capital was flowing easily.

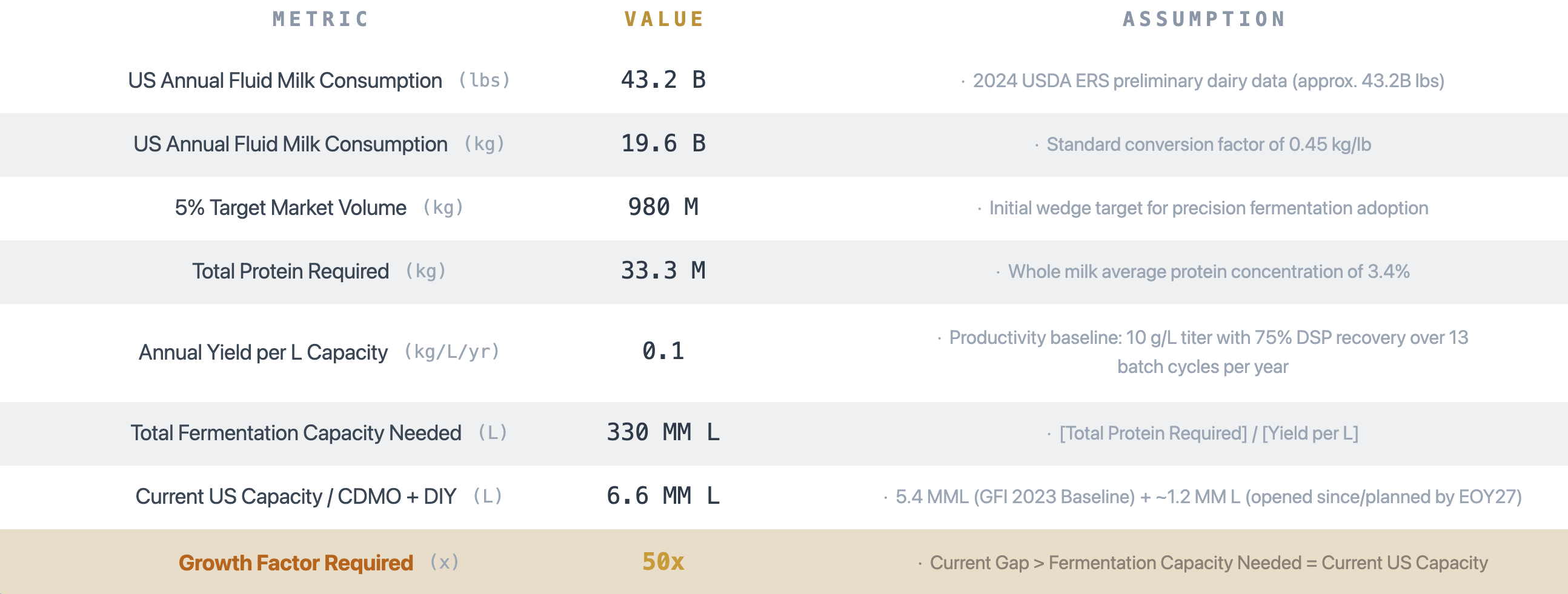

Table 1: US Fermentation Capacity Gap | Dairy Protein

Validating more multi-tenant capacity is essential for fermented proteins. Why? In 2023, GFI identified4 5.4M liters (L) of food-specific fermentation capacity in North America, of which only 1.8M L was for CDMO/CMOs. The rest was attributed to companies serving their own needs. We conservatively estimate that by EOY27, total capacity will be 6.6M L, inclusive of pre-announced facilities.5 At current titer, recovery, and utilization levels, the sector would need to expand roughly 50x (Table 1) to displace even a modest 5% wedge of the US fluid-milk sector.6 Hitting the industry’s cost-competitive efficiency targets shrinks that to 6x against total capacity. That reduction is the productivity gap repetitions close, and the flywheel this paper argues legibility funds. Absent forcing functions, getting more CDMO capacity built is a binding constraint. See Appendix A for assumptions.

Table 1: US Fermentation Capacity Gap | Dairy Protein

The 2026 Global Food Institute State of Fermentation report7 is measured in tone, leading with regulatory wins, new facilities, and precision fermentation’s growing share of sector funding. Read through a bankability lens though, it describes a doom loop with no obvious exit. High production costs force premium pricing. Premium pricing suppresses demand. Suppressed demand prevents the scale needed to build bankable infrastructure. Without bankable infrastructure, unit economics stay high.

The reflexive answer: go asset-light, partner with CPGs, lock in offtake, and prove demand. But taste or perception aren’t the only things to solve. The path also needs more CDMOs, more rentable capacity, more repetitions. More of the right infrastructure, not less.

2. Breaking the Doom Loop

I am new to this space and writing in public because the argument or conclusions may be wrong. If you want to argue back, the form is here.

This paper argues the bottleneck in alternative protein isn’t just biology, and it isn’t that demand is missing. It’s that capacity can’t be priced into the bankable offtake that demand could become. That’s a problem of financial legibility. The industry has not yet defined standardized units of work, which invites opaque pricing and discourages pricing-model optionality. That prevents capacity in its current form, the liters of bioreactor and DSP train time that fermentation-protein companies rent, from being priced, compared, or underwritten the way infrastructure assets are in mature sectors. The CDMO capacity that does exist is largely single-tenant, making it harder to re-market when a contract lapses, so even built liters carry less of the resale value capital underwrites against.

For precision fermentation to win, the industry has to name what it sells, show what it costs, and offer more than one way to buy it. Done precisely, a CDMO can aggregate a fragmented long tail of buyers, on-demand and prepaid alike, into the contracted offtake capital underwrites. Legibility sits upstream of supply: it is how more multi-tenant capacity gets built and provides a structure that bends the cost curve for anchor customer and startup alike. This financing gap isn’t structural. The conditions blocking the capital are specific and addressable, and a CDMO willing to build differently can remove them.

There is an intervention that can break this doom loop. The alternative protein industry needs to pursue three things in parallel: defined primitives, public pricing, and pricing-model variability. I call this bundle the Protein Fabric. The rest of this paper turns it into a framework: a method to generate and choose primitives across three stages of precision fermentation production, feedstock and strain engineering, fermentation, and DSP, then a way to meter, price, and sell those units of work. To bring it to life, we’ll also illustrate how Protein Fabric would surface publicly via a CDMO pricing prototype.

This framework is repeatable; practitioners in other infrastructure sectors can run this methodology for their production processes. To be clear, the paper does not claim primitives or public pricing magically solve taste or unlock debt capital. They won’t. Instead, read this as one viable and durable approach to introduce financial legibility, and get the fermentation flywheel spinning.

3. Protein Fabric Framework

Power, commodity chemicals, cloud, semiconductors, even the US Postal Service. Each one arrived at the same realization before it could scale, that it needed primitives, pricing transparency and pricing-model variability. Precision and biomass fermentation are next.

Primitives: A primitive is the smallest unit of something that retains meaning on its own and can be combined with others without losing meaning. A common set of underlying criteria are below. Primitives:

Atomic: Cannot be subdivided further within a domain;

Composable: Can be combined with other primitives to form larger structures or abstractions.

Distinct: Do not overlap with each other; they are unique dimensions of a domain.

Durable: Persist over time, making them stable to build upon.

Context-Independent: Core behavior does not change depending on what the primitive is paired with.

When primitives are defined, complexity decomposes: downstream actions become specifiable, risk attributable, and comparisons become possible. Primitives are not just capacity; some are events, measurements, units, or states others rely on. They can be bundled, abstracted, or transferred between parties. Without them, everything stays custom. Each transaction renegotiates units of work, comparisons fail, and sales conversations reinvent vocabulary that should be consistent.

Primitives emerge when standardization yields more benefit to the industry than any one party can capture alone. Once named the examples are obvious, the shipping container, the kilowatt-hour, the rail gauge, the postage class. Fermentation has no publicly defined primitive set where money flows, though, as we’ll see, it does have unlabeled examples.

Public Pricing: One of the most mundane and powerful moves a business can make is to publish its pricing. What matters commercially is pricing any buyer can see without a sales call, whether a consumer, a business, or an agent, attached to a unit of work (a primitive) that performs consistently across customers. The unit is named, the value declared, the meter consistent, and a web search or API call returns the same number for a like query, regardless of who is asking.8

When pricing becomes public, buyers model costs independently and lenders gain a curve to underwrite against. An MSA gives one buyer a private number after signing; it gives the market no curve and a lender nothing to compare. Public pricing also forces line items to be defended or removed, where opacity lets undefended margin survive. That is why the public path, not only private negotiation, scales the sector.

Pricing-Model Variability: It’s important not to confuse a pricing dimension (what you buy) with a pricing model (how you pay). Today, CDMOs bill across any number of dimensions, including fee for service, labor hours, per-batch, per-volume, and wraps them inside take-or-pay inside customized contracts. What’s uncommon is the pricing-model diversity that industries with primitives rely on. Different models can serve different buyer profiles and produce diverse revenue shapes for sellers. On-demand revenue is spiky and episodic, and it serves a long tail of use cases. Reserved revenue is contracted ahead of time. CDMOs already convert forward intent into contracted revenue through LOIs and MSAs, so commitment isn’t the missing piece. What a lender cannot do is generalize from a single private rate: one signed number says what one buyer paid, not what the next vessel earns. A posted on-demand and reserved curve answers that question; a contract drawer does not. Pricing-model diversity, not transparency alone, is the condition for infrastructure-grade capital.

A research scan of 100+ suppliers9 from GFI’s database10 revealed three themes. Some private CDMOs name a flexible pricing model but attach no number (campaigning and pay-per-kilogram / take-or-pay at Liberation). Ginkgo Bioworks, the closest thing to an “AWS of biology,” posts some public per-unit prices but at a different layer (assays and expression, not fermentation capacity). Publicly-funded university facilities post rate cards (Cornell, Alberta, AURI), but priced on conventional axes of labor, per-test fee, facility-time, or cost-share. The majority of U.S. providers follow a “contact us” model. Thus, examples of the pieces exist, but have never been assembled as Protein Fabric envisions. The consequence cascades. Seed-stage, B-round, and enterprises: few can model COGS reliably, and lenders can’t underwrite throughput against prices they can’t see. When the conventional wisdom is that techno-economic analyses are too optimistic, that’s powerful. The TEAs aren’t wrong because smart people aren’t modeling. They’re wrong because the inputs and assumptions are private.

4. AWS as an Illustration

With the Protein Fabric established, it’s worth looking at one company that built a wholly new business on a similar foundation.[1] What follows is an illustration, not a precedent. Fermentation is not software, but the commercial architecture is portable.

AWS launched in 2006 with S3 (storage), soon followed by EC2 (compute). It passes every primitive criterion: atomic, composable, distinct, durable (customers today still use the original API), and context-independent. The launch press11 release described S3 as “a simple storage service... at very low costs,” posted the price ($0.15/GB-month stored, $0.20/GB transferred), and set no minimum fee. Developers paid only for what they used. The primitive, public price, and pay-as-you-go model went live simultaneously, no sales conversation required. This broke how incumbents had sold enterprise IT for decades. Multi-year agreements, sales cycles measured in quarters, and hidden scaling costs. Incumbents spent the next decade reacting to AWS, whose customers didn’t have to call sales.

That was the start. As customers built on S3 and EC2, they asked for purchasing models beyond on-demand. EC2 Reserved Instances12 followed: a 1- or 3-year commitment for 30-60% off on-demand, giving CFOs a way to budget predictable cloud spend, while Spot instances offered steeper discounts to customers whose workloads could tolerate interruption. RIs also buffered AWS’s own revenue against customer spikiness and became a capacity-management tool. The pricing model wasn’t just a customer feature; it was the mechanism that made AWS scalable. The same primitive (an EC2 instance) was sold across multiple pricing models to three buyer profiles, without breaking the unit.

None of this was inevitable. At each step there were debates, including competitive reaction to public prices and whether new products would cannibalize revenue. The commercial architecture wasn’t designed up front. It was built iteratively with customers on top of extensible primitives and public pricing.

What follows is the precision and biomass fermentation version of that catalog.

5. From Candidates to Primitives

The first four sections made the case for Protein Fabric. What none of those sections did was explain how to actually pick primitives. That is the job of this section: a repeatable method any fermentation operator can run on their own to generate, qualify, and select the units of work the business will commit to.

To bring the Protein Fabric to life, let’s introduce two fictional entities: Otto, a food-grade CDMO selling precision/biomass fermentation services and Container Bio, a precision fermentation startup with a target protein looking for a CDMO to validate their approach. We’ll refer to both throughout.

Tenets: Defining what a primitive is does not tell you which primitives to choose. The selection mechanism is a set of tenets applied to each qualified candidate. Tenets are tiebreakers: precise enough to settle a question on their own, durable enough to last as the product changes. The tenets below are Otto’s. Another operator running this method should write their own.

Fermentation Primitive Tenets:

Zone of Control: Primitives are always within Otto’s control, something Otto can commit to and be held at the boundary it owns.

Deliverability: Otto commits to the envelope, not the result that emerges from it. A biological outcome co-produced with the customer’s strain cannot be solely attributed to either party after the fact, so it is not a primitive.

Attributability: Otto’s primitives make the failure boundary self-evident.

Portability: Otto’s primitive must survive domain translation. A primitive must mean the same thing as you vary feedstock, DSP trains, or organisms. Where the physics differs, the difference shows up as a variant of the primitive, not a new primitive.

Measurable: Otto’s primitives must be metered unambiguously at the point of delivery.

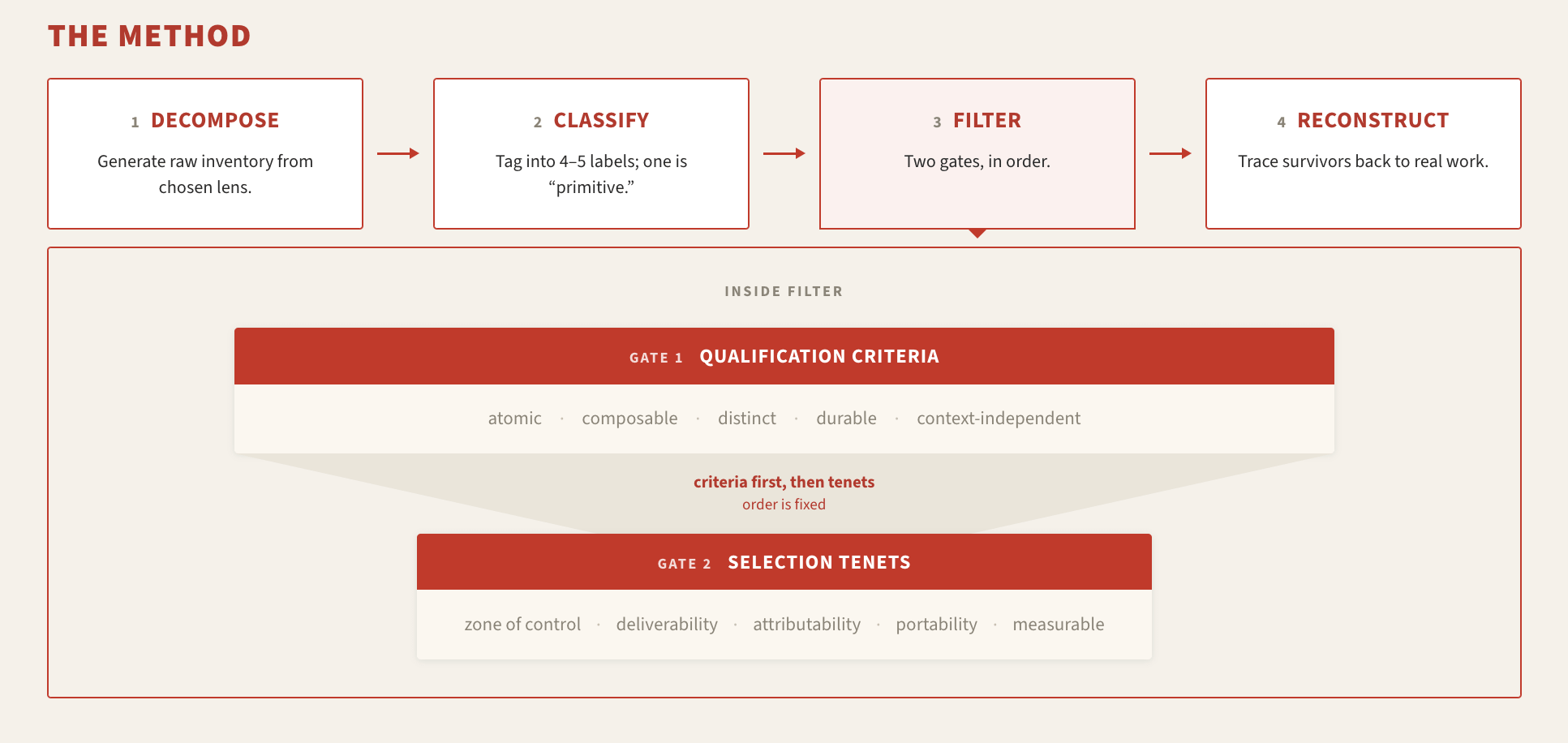

Running the Method: The procedure that applies the criteria and tenets to select primitives runs in four steps: 1/Decompose → 2/Classify → 3/Filter → 4/Reconstruct.

Step 1 (Decompose): This step generates a raw inventory of what units of work exist. Break the product or capability down from first principles. The generators you use depend on your lens: a commercial view (what already gets invoiced), a science view, persistent states and ownership boundaries, or process steps are all good starting points. Whatever generators you pick, add one pass no single lens provides: a sanity check that walks the draft inventory against varied conditions, different inputs, hosts, or equipment, to catch the units a single example would miss.

Step 2 (Classify): Now take this blob of ideas and generate 4-5 labels, one of which is ‘primitive’. This adds structure to your inventory via tags, but does not remove items. Every label except primitive is disposable. Tags are assumptions, not gates.

Table 2 | The Method

Step 3 (Filter): There are two filter passes, done in order. First, determine if each primitive candidate satisfies all of the qualification criteria. Then take those that pass and apply the selection tenets. This is where narrowing starts. Expect surprises and imposters: candidates that look like primitives but turn out otherwise.

Step 4 (Reconstruct): The final step inverts the decomposition. Working backward from each surviving primitive to the source material from Step 1, confirm it traces to a real unit of work. A primitive that traces to nothing is a phantom and gets cut. The output is a clean set of primitives and their sub-types (e.g., soda: cherry, orange, plain).

The next few sections run the method across all three fermentation production stages. They are the proof that it ports, and they are where to go deep dive into primitive choices. A reader who wants the commercial payoff can jump to Section 10; the result is the same primitive set, now priced.

6. Feedstock and Strain Primitives

The feedstock and strain engineering stages perform four main functions: identify and validate an organism capable of industrial-scale expression; bank that organism as a stable, genetically consistent asset; engineer and optimize carbon and nutrient streams specific to that organism’s metabolism; and transfer the validated inoculum (starter) to a fermentation vessel at a declared specification.

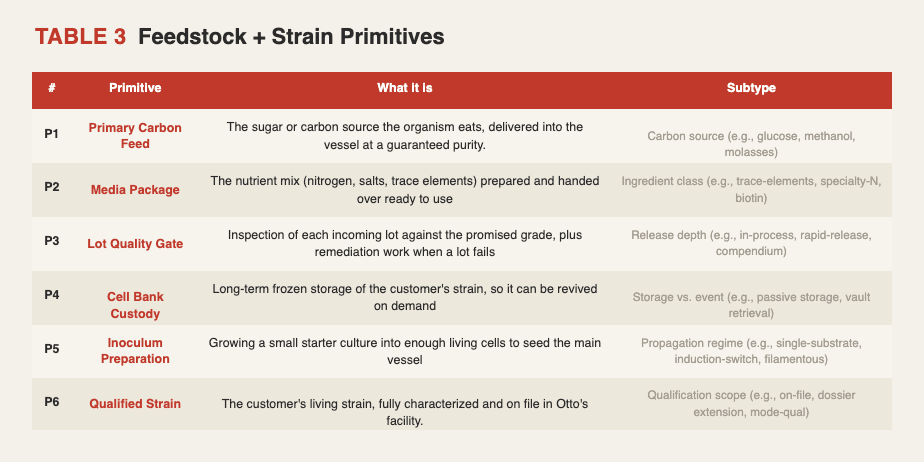

Step 1 (Decompose). For Otto, we generate the inventory from the commercial lens where money already flows: the invoice Container Bio would get from Otto, the unpriced costs Otto absorbs or provides for free, and the sanity-check pass from Section 5, run here across different organism/feedstock pairings to confirm candidates hold up beyond a single host. With these inputs, we identified 18 candidates, among them media sterilization, in-run supplementation, strain qualification, the carbon substrate itself, and cell bank storage.13 A note on sourcing. Otto is fictional, so there is no invoice to point at. Instead, Otto’s invoice is synthesized from publicly available information on food-grade CDMOs.14 These buckets are mine, and I treat them as a defensible starting point, not ground truth.

Steps 2 through 4 (Classify, Filter, Reconstruct). We classified the 18 candidates, filtered them against the criteria and then the tenets, and reconstructed the survivors back to cost inputs without gaps or duplicates, yielding a final list of six primitives (Table 3). The eliminations worth walking are the ones that taught the framework something, and they follow below. One important learning concerns primitive “sub-types.” A sub-type is not a new primitive. It is the same primitive with a variant, akin to a cloud customer picking a different GPU type for inference versus training: both are compute, not a new primitive. Where a primitive has “sub-types”, visible in the variant column, they are split by an infrastructure dimension Otto configures differently, not biological taxonomy. Inoculum Preparation splits by propagation regime (single-substrate, induction-switch, filamentous-morphology) because a methanol-fed Pichia and a molasses-fed S. cerevisiae are both yeast, but demand different seed-train infrastructure, hence different sub-types.

Take Tech Transfer, a common part of contract manufacturing agreements. The Tech Transfer process (and package) is how Otto gets a customer’s strain qualified and run through their infrastructure. It passes three of the five criteria (distinct, durable, atomic) but fails composability: it has constituent parts Otto already meters separately, a qualified strain, labor, and vessel time for runs. It is not a fourth thing alongside them; it is a project wrapper around the other three. So when a lender asks how much Tech Transfer revenue is strain readiness vs. facility time vs. expert hours, the answer shifts, because the underlying primitives are collapsed and cannot be repriced when the mix changes.

Now, we focus on a survivor, the Qualified Strain, the clearest case of a primitive that is a state rather than an action. Qualification work happens per strain (characterization, robustness, release panel, filed dossier) and the qualified state persists. Every campaign after the first reads from it: Inoculum Preparation inherits temperature bands and shear limits; Lot Quality Gate inherits identity panels and release specs; and Cell Bank Custody references the characterization baseline. Without Qualified Strain, each would re-contract the biology on every batch. A project has start and end dates. A qualified strain has neither, just a record other primitives read from. How Otto meters that state, a project fee, a per-event charge, is its commercial choice, not a fact of the biology, which is the lever Section 10 pulls.

In the next few sections, we show how fermentation and DSP primitives are harder tests: capital intensity is higher, sub-type proliferation spikes, and the organism classes Otto supports create more pressure on the infrastructure-not-biology cut.

7. Fermentation Primitives

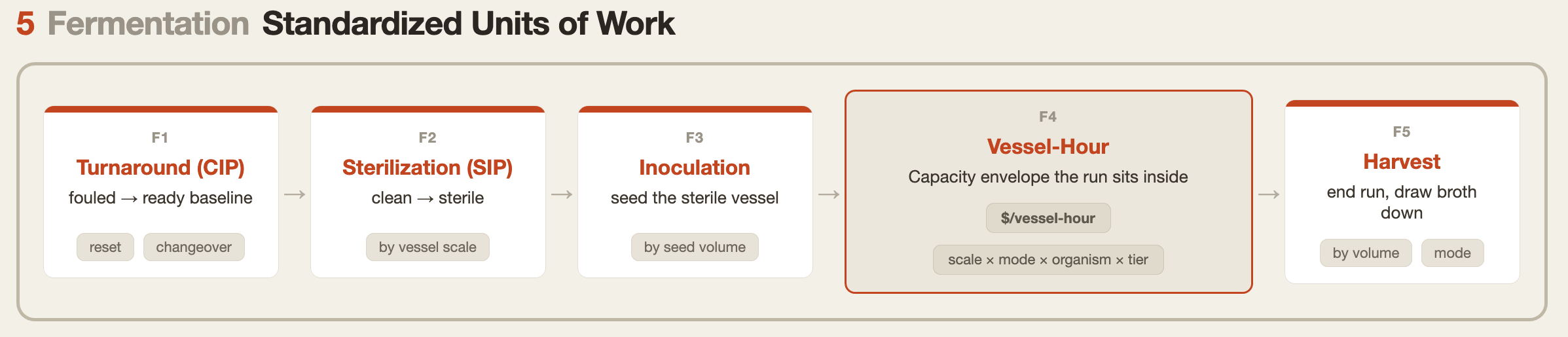

Fermentation is where the framework meets things that are scheduled, capitalized, and real but still not primitives. A run is a sequence of steps: sterilize the vessel, inoculate, hold a controlled envelope (temperature, dissolved oxygen, pH, agitation), then harvest. Each step is infrastructure Otto maintains at the vessel boundary, the scaffolding around a variable biological core.

We run the same four-step method; decomposing this stage from first principles starts with a more robust set of 2115 candidates, the ones a CDMO operator would list if asked what they actually sell time on. After classify, filter, and reconstruct, five fermentation-specific primitives survive. Several recurring lines here are not fermentation primitives at all, among them an offline assay and a utility draw; because they reappear in multiple stages. We collect them in the Shared Meters section. The rest of this section walks three eliminations that taught the framework, plus the survivor we initially missed.

The first candidate to stress the framework is the seed train, where vessels of progressive sizes (2L -> 20L -> 200L -> …) scale biomass up to production size before the main vessel is inoculated. My hypothesis is that CDMOs will want this as a primitive: seed capacity is scheduled, utilized, and constrained; customers must wait for it. Yet, it’s not a primitive. Seed train is several existing primitives bundled (vessel hours + media + a starter culture). The output is qualified inoculum, which is already a primitive in the Feedstock/Strain section. A seed train isn’t a new primitive; it’s additional usage of an existing primitive.

The second stressor groups candidates which are run-time actions: fed-batch carbon additions, nutrient top-ups, and additives like antifoam and pH trim. These happen inside the vessel, during the run, on the CDMO’s watch, thus, they feel natural as primitive. But these fail the non-uniqueness criteria; we already see these as existing primitives in the Feedstock/Strain section. A fed-batch carbon addition is the carbon feed delivery meter firing. Nutrient, antifoam, and pH trim additions relate to the media package primitive being used again. Nothing about them changes because they occur at a different production stage. A primitive exists once; without that prior-existence check, you double-count what the customer already pays for.

The third anti-pattern relates to the canonical metrics of a fermentation run. These are: growth rate (μ) plus titer, rate/productivity, and yield (TRY). Originally, we thought at least titer would survive. However, the Zone of Control and Deliverability tenets draw the line; Otto delivers the infrastructure and is held to it, but does not absorb what the customer’s biology controls. Otto’s kLa, feed execution, and scale-down model shape titer, but influence is not ownership. Run two strains in the same held envelope and they reach different titers; the difference belongs to the customer’s strain, media, and process, not the vessel. That is why titer is reportable, not committable: the envelope can be priced, the outcome should not. Today, CDMOs run per-batch pricing, quoted against a declared titer assumption, and when the strain underperforms, the customer’s per-gram cost rises. Stating the boundary this way codifies existing practice rather than imposing a new one.

The candidate that taught the most is the one we almost dropped: vessel turnaround, the clean-in-place (CIP) cycle that returns a fouled vessel to a clean, ready-to-sterilize baseline for the next customer. It stops at that clean baseline; the steam-in-place (SIP) cycle that takes the vessel from clean to sterile is a separate sterilization event. In a single-tenant frame turnaround is invisible overhead, folded into vessel-hour economics. Multi-tenancy is what surfaces it: the cost of switching from one product to the next varies with how different they are, a same-product reset is a short CIP while a switch across organism classes demands cleaning to a validated threshold and re-qualification, and that cost should fall on whoever triggers it. It is atomic, composable, distinct, and squarely in Otto’s Zone of Control, since unlike a failed batch it needs no customer arbitration. Pricing it is what makes shared capacity financeable.

Finally, vessel-hour teaches something else. A vessel-hour isn’t a single thing. A 2L bench vessel and a 150,000L production vessel both bill “vessel-hours” at prices differing by orders of magnitude, fermentation mode, organism class, and performance tier. It is a family, not a single rate; how a CDMO prices it comes later.

Five fermentation primitives remain, each owning one transition with no overlap into the next: turnaround cleans, sterilization sterilizes, inoculation starts, harvest ends, and vessel-hour is the capacity state they all sit inside, itself a family rather than a single rate, varying by scale, fermentation mode, organism class, and performance tier.

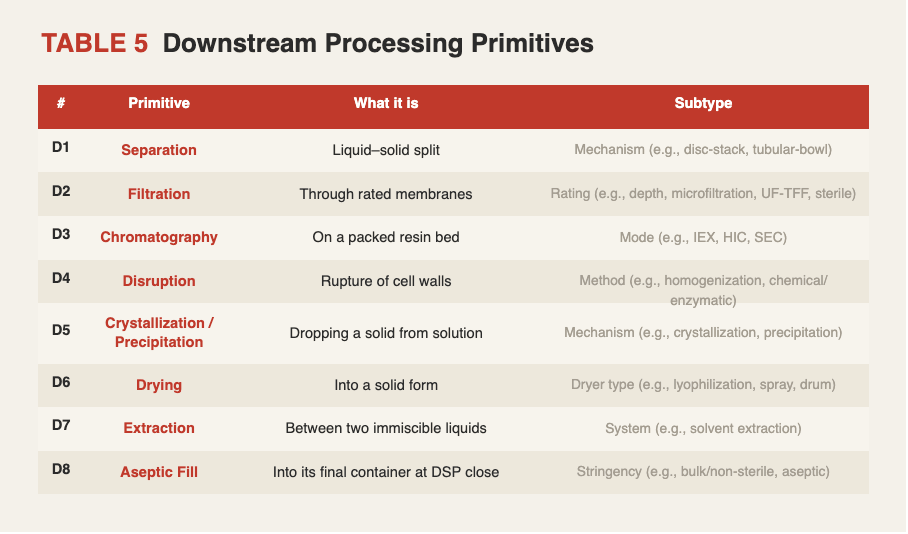

8. DSP Primitives

Downstream processing is where the broth that leaves the fermenter becomes product. It moves through a sequence of operations: separating cells from liquid (or rupturing if intracellular), removing debris, capturing target proteins, polishing, sterilizing, and in some campaigns, filling into containers. DSP campaigns are heavily impacted by fermentation TRY outcomes. If TRY lands below target, the DSP sequence remains, but each step carries a “TRY tax”, i.e., longer durations to reach the same yield, additional filtration passes, extra polish, and so on.

My first instinct was to build primitives based on DSP stages, clarification, capture, et al., since each one feels like a unit of work. They aren’t. A stage is a position in the sequence, not a kind of work. Take filtration, it recurs in clarification, in polishing, in concentration, and in the sterile step. If stages were primitives, that one operation would fracture into four. Instead it is a single primitive with sub-types that differ by physics (depth, TFF, nanofiltration, sterile), not by where they sit in the run. Unlike fermentation which is a process you judge by an aggregate outcome (TRY), DSP breaks at the edges between operations, where each one has discrete inputs, outputs, and pass/fail criteria. Those edges are where the work actually divides, and cutting on them lets each primitive answer to its own physics.

We run the same method again, this time starting with 26 candidates.16 As before, several candidates fall away at the first filter, the qualification criteria, which ask whether a thing is even a clean, standalone building block. The surprise came at the second filter. The selection tenets, the rules that decide whether a building block is something Otto can actually stand behind and put a price on, dropped nothing.

That was puzzling, until the reason became clear. In fermentation, that second filter does real work, because the outcome of biology is never fully in the provider’s control. DSP is a different animal. Here chemistry and physics do the work: pumps, filters, columns, dryers, each with a defined input, a defined output, and a clear pass or fail. The unpredictable part, the biology, happened upstream in the fermenter. By the time material reaches downstream processing, no candidate shows up as a biological-outcome question, so none of them trip the tenet built to catch one. Of the original 26 candidates, eight survive (Table 5).

9. Shared Meters

The cut between a primitive and a shared meter is ownership of work. Three items recur across the framework without belonging to any single stage: parts of each stage merely draws down the same input, that is a shared meter, declared once and invoked anywhere. Utility charges (e.g., electricity, steam, water) span every stage that powers equipment. An Assay Unit (AU) is a measurement producing an answer the customer can act on, so a fermentation titer check and a DSP release test are the same meter measuring different actions. A Consumable Consumption Unit (CCU) is a normalized unit of pass-through: undifferentiated material Otto buys and passes through with an uplift.

Across three stages we identified 19 primitives and three shared meters, a reasonable set for mapping a whole CDMO’s business. One tip for teams newer to primitives: most over-classify at first and resist cutting. When in doubt, cut. The north star is the smallest set that runs your business at a high bar.

10. Pricing

Section 3 argued that public pricing and pricing-model variability matter. Public pricing makes the unit visible; variability makes that same unit sellable in different revenue shapes, so a lender can underwrite against a reserved floor instead of trusting a private model. Neither guarantees demand. What they do though is lessen uncertainty, the precondition.

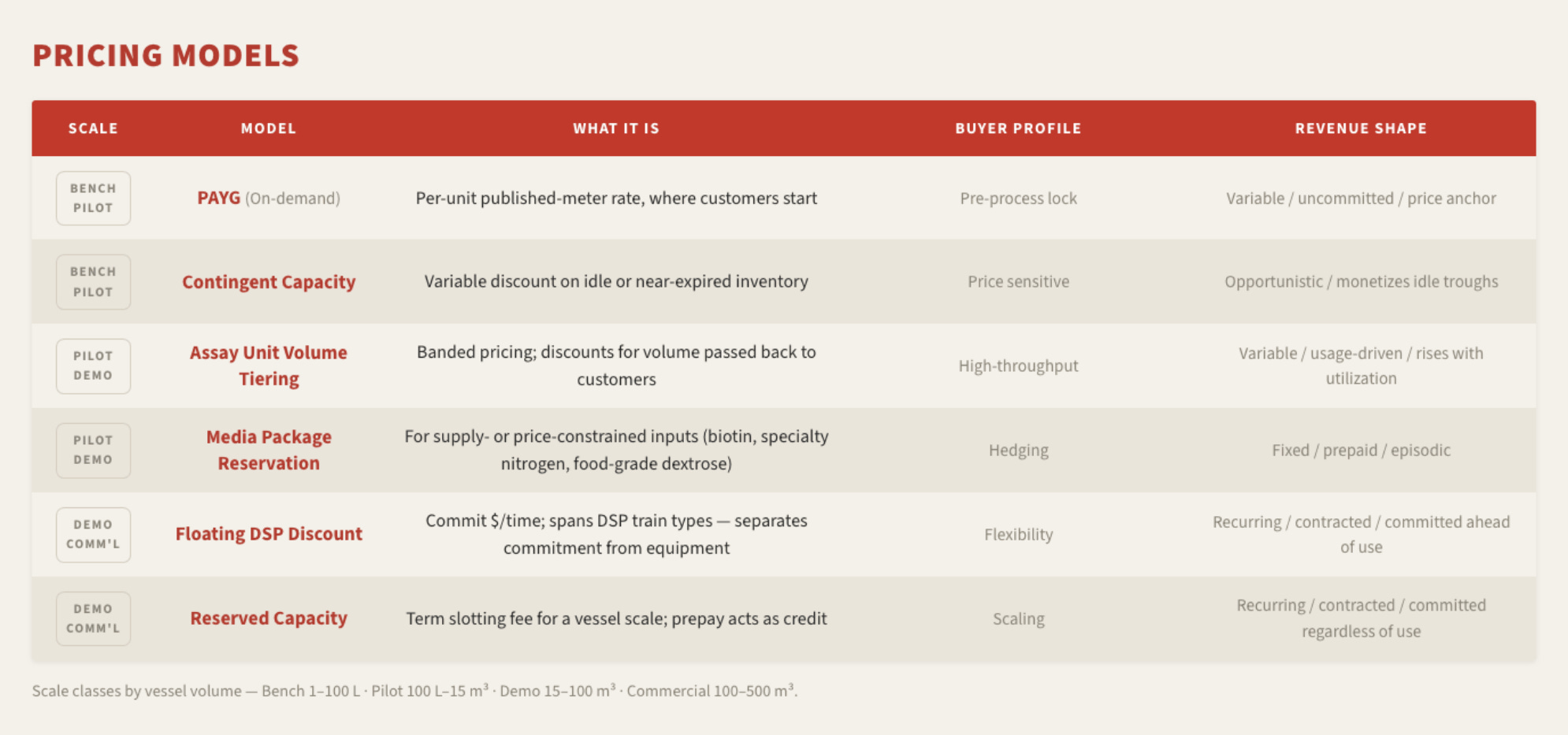

We argue pay-as-you-go (PAYG) is the right starting point for fermentation primitive pricing. PAYG should not be confused with “cheapest.” Its power is that it removes friction other models impose: a reservation needs a forecast and a commitment, while PAYG needs a rate, meter, and payment method. A buyer can transact before any relationship exists. It also becomes the reference other models key off, since discounts are expressed against the on-demand rate. PAYG is also purpose fit for a buyer that isn’t ready to forecast or who needs a pilot to understand where first titer lands.

Reservations and commitments come next, each serving a buyer behavior PAYG does not. The below are illustrative; a real CDMO would tune them to its own equipment, product mix, and financial goals.

Reserved Capacity. A slotting fee for a specific vessel scale over a fixed term, paid regardless of utilization, in exchange for a discount off the on-demand rate. It also includes pre-payment options, which serve as a credit mechanism. A prepaid or escrowed reservation is bankable independent of the buyer’s credit because cash is in hand, while a no-upfront one is only as good as the counterparty. A CDMO wanting its reserved book to count as a financeable floor prices the upfront variants to pull buyers toward prepayment.

Floating DSP Discount. Customers commit a dollar amount per unit of time, and the discount applies across DSP train types rather than a single asset. This separates the financial instrument (the commitment) from the capacity instrument (the equipment). A customer whose process shifts from centrifugation to filtration keeps the discount.

Assay Unit Volume Tiering. Banded pricing, falling as monthly campaign volumes rise. The band prices pass back a decline in the CDMO’s average (fully-loaded) cost per assay, the fixed instrument amortized across more samples and higher utilization.

Media Package Reservation. Applied to supply- or price-constrained inputs (e.g., biotin, specialty nitrogen sources, food-grade dextrose, ammonia). A customer reserves supply and consumption meters at a fixed rate, converting uncertainty into a priced commitment.

Contingent capacity. A variable discount on idle capacity or near-expired inventory, offered for non-critical development or pilot runs that can tolerate the terms.

A mixed book turns one asset into several products: reserved and floating commitments contract revenue ahead of use, tiering and contingent capacity monetize idle time, and the demand signal lowers the cost of capital. For the customer it means matching commitment to confidence and running experiments a project-fee quote would kill.

See it priced. Every primitive and pricing model in this paper is live in an interactive rate card. Set a volume, pick a model, watch the number move.To make this tangible -> open the prototype

11. Pushback

It’s worth making the flywheel explicit, as the title promises. Posted primitives and varied pricing models widen the funnel, and that granular demand fills the troughs anchor-only customers leave when they depart. Utilization is repetitions, and repetitions bend the cost curve. As it bends, the delivered price falls toward what a CPG off-taker can consider, that contracted offtake is what capital underwrites, and cheaper capital aids facility expansion. Each turn happens without renegotiating the unit of work from scratch. Protein Fabric makes a claim about how fermentation services should be priced and sold. The honest test of a claim is its falsifier, so what would have to be true for this one to fail?

The first objection says standardization isn’t necessary to attract capital. Venture and debt already fund fermentation, and a toll road gets financed without a primitive. That’s fair: a lender underwrites contracted cash flows, counterparty credit, and recovery value, not a public rate card. But that locates the real work. Two questions hide inside “is it financeable?” Can a lender underwrite construction debt, which needs contracted, creditworthy offtake, and can the CDMO get the utilization to drive unit economics? The toll road answers the first. The doom loop lives in the second, where a CPG won’t sign until prices drops and the prices won’t drop without repetitions. That second job is legibility’s, and it sits upstream of supply. Posted primitives and varied pricing models let a CDMO fill a vessel from a long(er) tail and a reserved mid-market alongside anchors, and that contracted offtake is what capital underwrites, not the rate card.

The fair pushback is that a reservation from a pre-revenue startup is a soft promise. Two things make it collateral: prepaid reservations are bankable regardless of credit because the cash is in hand, and a standardized unit is resellable, so a defaulted slot resells into the same curve and a failed platform leaves the lender a standard asset rather than a stranded single-product line. Initial funding is likely equity, grants, or anchor money, not project debt, so I’m not claiming a rate card raises construction debt; I’m claiming it manufactures the offtake that does. What would prove me wrong? If shared capacity gets financed like a single toll road, one asset, one investment-grade off-taker, take-or-pay, no posted prices, and the industry massively scales, then legibility was never a blocker.

The second objection, in its sharpest CFO form, is that posting prices first is unilateral disarmament. It anchors every prospect, loses customers that quietly opt out, and invites undercutting. The standardization benefits accrue to the industry while exposure falls on the first mover. The conclusion is backwards. Transparency is a one-way door, so the trap isn’t going first; it’s being third or fourth after a competitor posts, defines the units everyone compares on, and routes the inbound funnel to itself. Going first sets the market, the standard becomes yours, and competition moves up the stack to reservations, reliability, and support. What would prove me wrong: a credible operator posts, durably loses share to opaque incumbents, and no one follows. I think the opposite occurs.

The third objection may be the strongest: alternative proteins are not yet comparable to conventional peers on taste or price, and no amount of capital legibility changes that. I can’t argue otherwise. Legibility does not fix demand. It does stop the sector from mistaking “willing to try” for “willing to buy.” Honest primitives feed more accurate TEAs, so capital gets deployed against real unit economics instead of inflated ones, and demand signals get priced correctly. That is a benefit, not a cure. Now, if demand never materializes at prices rivaling conventional proteins, then the sector isn’t durable as a business.

12. Conclusion

The intervention this paper proposes is repeatable. Decompose a production process into standardized primitives, then make them legible to capital: named and metered, priced in public, and buy-able in more than one shape. The method ports to any infrastructure sector, not just fermentation.

Applied here, it yields a primitive set across feedstock and strain, fermentation, and DSP, plus shared meters across. Made public and priced across models, those primitives turn opaque capacity into something a lender can underwrite and a buyer can model. Legibility first, capital after, a market that can compare, aggregate, and finance rather than renegotiate every transaction from scratch.

A caveat: I am new to this space, and I am writing in public because the argument may be wrong. The primitive choices could be wrong, the pricing models impractical, biological randomness enough to blunt the whole thing. This is a proposed path, not a guaranteed blueprint. If you think I’ve got something wrong, this short form is where to tell me.

Appendix A – Methodological Notes & Model Assumptions

1. Macro Market Baselines & Conversions

· US Fluid Milk Footprint: Total baseline volume is established at 43.2B lbs, utilizing the 2024 USDA Economic Research Service (ERS) preliminary dairy summary data for fluid milk products.

· Mass Normalization: To maintain cross-commodity analytical parity, imperial measurements are converted to metric utilizing a standard factor:

43,200,000,000 lbs × 0.453592 kg/lb = 19,595,171,700 kg

· Target Market Wedge: The model targets a 5% displacement of fluid volume (979,758,585 kg of milk equivalent) as an initial, market-entry penetration vector for precision fermentation adoption.

2. Protein Concentration & Mass Balances

· Dairy Protein Density: Pure whole milk is modeled at an average structural protein concentration of 3.4% by weight (representing a composite baseline of caseins and whey proteins, such as β-lactoglobulin).

· Total Target Output: The net mass of pure, dry protein required to substitute the 5% fluid milk wedge is calculated as:

979,758,585 kg × 0.034 = 33,311,792 kg

3. Bioprocess Engineering & Annual Yield Model

· Upstream Fermentation Titer: Today the model uses roughly 10 g/L (0.010 kg/L), the hero value for demonstrated secreted food-protein titers (Nielsen et al., 2024), against a demonstrated fleet nearer 5 g/L. The mature case uses 51 g/L (0.051 kg/L), the cost-viability target that same literature states, not a current fleet value. Both apply to hyper-expressing filamentous fungi (Trichoderma reesei) or methylotrophic yeast (Pichia pastoris) platforms before extraction.

· Downstream Processing (DSP) Efficiency: A 75% net DSP recovery efficiency is applied in both regimes, avoiding the error of assuming 100% recovery. This accounts for unavoidable mechanical, purification, and crystallization mass losses across industrial separation trains (e.g., disc-stack centrifugation, ultrafiltration, and spray drying) while preserving core ingredient functionality.

Net recovered protein per batch: Today 0.010 kg/L × 0.75 = 0.0075 kg/L/batch; Mature 0.051 kg/L × 0.75 = 0.03825 kg/L/batch.

· Annual Facility Utilization: The model assumes 13 complete batch cycles per vessel-year today, against frequent changeover and unplanned downtime, rising to 22 at maturity with short repeated turnaround. The mature cadence reflects an average cycle near 7 days: a 90 to 120 hour fed-batch run, then 36 to 48 hours for harvest draw-down, CIP, and the separate SIP sterilization cycle, with headroom for annual mechanical maintenance, contamination events, and downstream bottleneck idling.

4. Volumetric Capacity and Growth Factors

Net Volumetric Productivity Yield. Annual net yield equals titer times downstream recovery times batches per year. We carry both regimes through the math, not just the mature target.

Today: 10 g/L titer × 75% recovery = 0.0075 kg/L per batch; × 13 batches/year ≈ 0.10 kg/L/year.

Mature: 51 g/L titer × 75% recovery = 0.03825 kg/L per batch; × 22 batches/year = 0.8415 kg/L/year.

Total Required Infrastructure Footprint. Displacing the 5% fluid-milk wedge requires 33.3M kg of protein. Dividing by each regime’s annual yield gives the active vessel volume that regime demands:

Today: 33,311,792 kg ÷ 0.10 kg/L/year ≈ 330M L.

Mature: 33,311,792 kg ÷ 0.8415 kg/L/year ≈ 39.6M L.

Current Infrastructure Baseline. Total active US food-grade fermentation capacity reaches 6.6M L by EOY27: a 5.4M L deconflicted baseline (the 2023 GFI census of North American food-grade capacity across all protein types) plus roughly 1.2M L opened since or explicitly planned through 2026 to 2027. We report against this total capacity, since protein from captive and own-use producers also displaces milk; the rentable multi-tenant subset is the tighter constraint a new entrant faces.

Resulting Growth Multiplier. Dividing the volume each regime demands by the 6.6M L available gives the multiple:

Today: 330M L ÷ 6.6M L ≈ 50x.

Mature: 39.6M L ÷ 6.6M L ≈ 6x.

Endnotes

[1] Until recently, the author had spent 11+ years at AWS, participated in many debates on primitives, pricing models, and transparency.

[1] https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001655210&type=10-Q, https://agfundernews.com/new-owner-of-meati-insists-brand-poised-for-growth-after-mass-layoffs-staff-say-theres-no-plan-just-a-shutdown-and-silence, https://agfundernews.com/breaking-believer-meats-ceases-operations-but-setback-does-not-mean-cultivated-meat-sector-is-doomed-insists-amps, https://agfundernews.com/exclusive-perfect-day-to-sell-consumer-brands-so-it-can-focus-on-b2b-operations

[2] https://www.nature.com/articles/s41538-024-00291-w; https://www.mckinsey.com/industries/agriculture/our-insights/ingredients-for-the-future-bringing-the-biotech-revolution-to-food

[3] https://www.synbiobeta.com/read/liberation-labs-rebrands-as-liberation-bioindustries-to-reflect-global-biomanufacturing-scale

[4] https://gfi.org/resource/fermentation-manufacturing-capacity-analysis/

[5] Excludes: pharma or other capacity, international (e.g., EU 3.6M/L CDMO capacity), or expansions may come online in 2028+.

[6] Capacity needed equals protein required (33.3M kg: 5% of US fluid milk at 43.2B lbs, 3.4% protein) divided by annual yield per liter (titer × 75% recovery × annual batches), measured against 6.6M L of projected EOY27 capacity. At today’s ~10 g/L titers and ~13 batches/yr (0.10 kg/L/yr) the gap is ~50x; at the 51 g/L viability target and 22 batches/yr (0.84 kg/L/yr) it falls to ~6x.

[7] https://gfi.org/wp-content/uploads/2026/04/GFI-2026-State-of-the-Industry-Fermentation-for-meat-seafood-eggs-dairy-and-ingredients.pdf

[8] An autonomous procurement agent reading a published price evaluates the same primitive against the same meter as a human does

[9] Examples are: Cornell Food Venture Center, Franklin County WMFPC, Alberta Food Centre, AURI, Berkeley ABPDU, BioMADE, Corden BioChem, Liberation Bioindustries, Cell Culture Co, AGC Biologics, 21st.BIO, Ginkgo Bioworks, Tanda, CytoNest, Ecovative.

[10] https://gfi.org/resource/alternative-protein-comp1any-database/

[11] https://press.aboutamazon.com/2006/3/amazon-web-services-launches

[12] https://aws.amazon.com/ec2/pricing/reserved-instances/

[13] Candidates that did not survive include feedstock remediation, strain process development, analytical method transfer, the tech transfer project, and strain-origin deviation investigation. The full inventory with first-principles reasoning is available on request.

[14] Evonik Fermas, Laurus Bio, Arxada, EnviroZyme, ScaleUp Bio

[15] Candidates that did not survive include the seed train, controlled additions such as antifoam and pH trim, online PAT monitoring, off-gas analysis, and TRY (titer, rate, yield). The full inventory is available on request.

[16] Candidates that did not survive include enzymatic and chemical lysis, refolding, DSP tech transfer, bead milling, and expanded bed adsorption. The full inventory is available on request.